Retirement may seem like a distant dream when you are in your 20s or 30s, but it is never too early to start saving for the future. However, life can get in the way, and many people find themselves behind on their retirement savings as they approach their golden years. If you find yourself in this situation, don’t panic. There are steps you can take to catch up on your retirement savings and ensure a comfortable and secure future.

Assess Your Current Financial Situation

The first step to catching up on your retirement savings is to assess your current financial situation. Take a close look at your income, expenses, and existing retirement accounts. Determine how much you are currently saving for retirement and whether it is enough to meet your goals. If you are behind on your savings, don’t worry. The important thing is to take action now to get back on track.

Create a Budget and Cut Costs

One of the most effective ways to catch up on retirement savings is to create a budget and cut costs. Look for areas where you can reduce your expenses, such as eating out less, canceling subscriptions you don’t use, or finding cheaper alternatives for everyday expenses. By trimming your budget and redirecting the savings towards your retirement account, you can make a significant impact on your savings over time.

Maximize Contributions to Retirement Accounts

Another way to catch up on retirement savings is to maximize your contributions to retirement accounts. If you have a 401(k) or IRA, consider increasing your contributions to the maximum allowed by the IRS. Take advantage of any employer matching contributions to boost your savings even further. By increasing your contributions now, you can make up for lost time and build a more secure retirement nest egg.

Consider Delaying Retirement

If you are behind on your retirement savings, you may need to consider delaying retirement. By working a few extra years, you can continue to save for retirement and allow your savings to grow. In addition, delaying retirement can increase your Social Security benefits and reduce the number of years you need to rely on your savings. While postponing retirement may not be ideal, it can provide financial security and peace of mind in the long run.

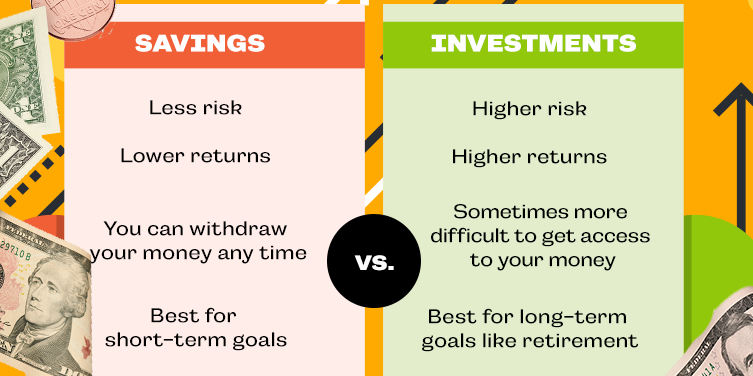

Invest Wisely

When catching up on retirement savings, it is essential to invest wisely. Consider diversifying your investment portfolio to minimize risk and maximize returns. Consult with a financial advisor to develop a sound investment strategy that aligns with your retirement goals and risk tolerance. By investing wisely and staying informed about market trends, you can make the most of your savings and secure a comfortable retirement.

Stay Committed to Your Goals

Above all, staying committed to your retirement savings goals is key to catching up on your savings. Make saving for retirement a priority and stay disciplined in your financial decisions. Monitor your progress regularly and adjust your savings strategy as needed. Remember that it is never too late to start saving for retirement, and every little bit helps. By taking control of your financial future now, you can ensure a secure and comfortable retirement down the road.

By following these steps and staying focused on your retirement goals, you can catch up on your savings and build a secure future for yourself and your loved ones. Remember that it is never too late to start saving for retirement, and with a proactive approach, you can enjoy a comfortable and stress-free retirement.