Managing personal finances can be a daunting task, especially in today’s fast-paced world. However, avoiding common mistakes can help you stay on track and achieve financial stability. In this article, we will discuss the top 5 mistakes people make with their personal finances and how you can avoid them.

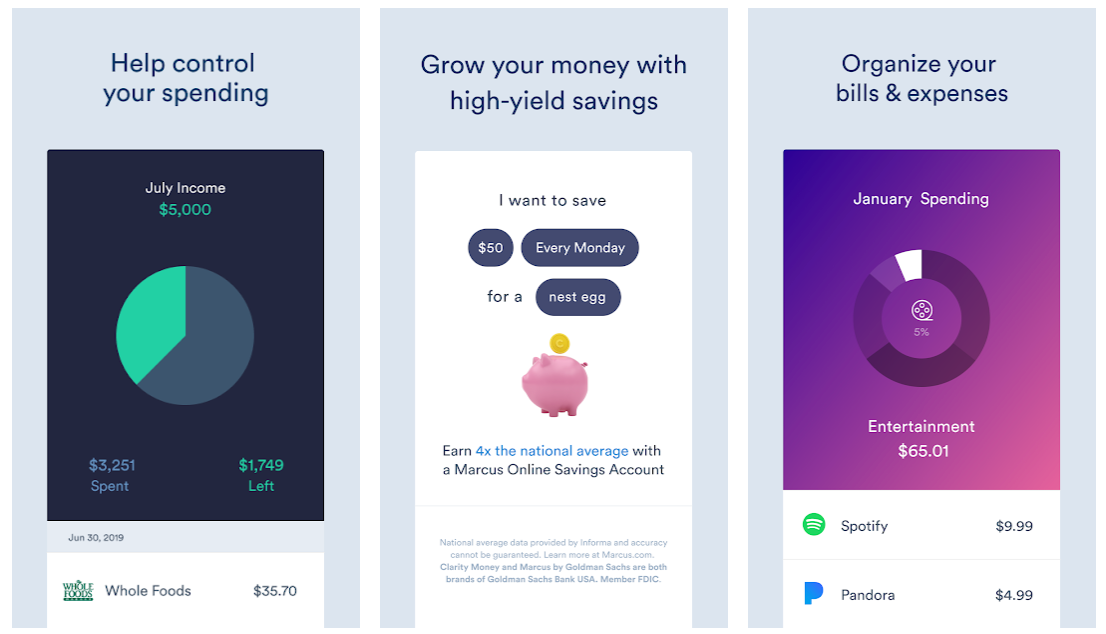

1. Not Having a Budget

One of the biggest mistakes people make with their personal finances is not having a budget. A budget is a roadmap for your spending and saving goals, and without one, it’s easy to overspend and lose track of where your money is going. Creating a budget allows you to prioritize your expenses, save for future goals, and avoid unnecessary debt.

2. Living Beyond Your Means

Another common mistake is living beyond your means. It can be tempting to spend money on luxuries and indulgences, but doing so can quickly lead to financial trouble. It’s important to live within your means and only spend what you can afford. This may require making sacrifices and cutting back on non-essential expenses, but it will ultimately lead to greater financial security.

3. Not Saving for Emergencies

Many people make the mistake of not saving for emergencies. Unexpected expenses can arise at any time, such as a medical emergency or car repairs, and having a financial safety net in place can help protect you from financial hardship. Aim to save at least 3-6 months’ worth of expenses in an emergency fund to cover any unexpected costs that may arise.

4. Ignoring Debt

Ignoring debt is another common mistake that can have serious consequences. Whether it’s credit card debt, student loans, or a mortgage, it’s important to prioritize paying off debt and not let it linger. High-interest debt can quickly spiral out of control and hinder your financial progress. Create a plan to pay off your debt systematically and avoid taking on additional debt whenever possible.

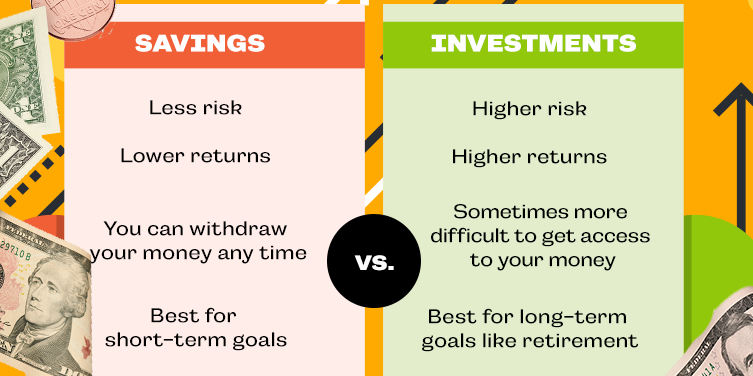

5. Not Investing for the Future

Lastly, not investing for the future is a mistake that many people make with their personal finances. Investing is essential for building wealth and achieving long-term financial goals. Whether it’s through a retirement account, stocks, or real estate, investing allows your money to grow over time and provide financial security in the future. Start investing early and regularly to take advantage of compound interest and maximize your returns.

Conclusion

Avoiding these top 5 mistakes with personal finances can help you take control of your financial future and achieve long-term financial stability. By creating a budget, living within your means, saving for emergencies, prioritizing debt repayment, and investing for the future, you can set yourself up for success and achieve your financial goals.