When it comes to saving for retirement, there are several options available to individuals. Two of the most popular choices are the Roth IRA and the Traditional IRA. Both retirement accounts offer tax advantages, but they have some key differences that can impact your retirement savings strategy. In this article, we will explore the pros and cons of each type of IRA to help you make an informed decision about which one is right for you.

Understanding the Basics

Before we dive into the pros and cons of Roth IRAs and Traditional IRAs, let’s first take a look at how each account works.

Roth IRA

A Roth IRA is a retirement account that allows you to contribute after-tax dollars. This means that you do not get a tax deduction for your contributions upfront, but your withdrawals in retirement are tax-free. Additionally, Roth IRAs do not have required minimum distributions (RMDs), so you can let your money grow tax-free for as long as you like.

Traditional IRA

A Traditional IRA is a retirement account that allows you to contribute pre-tax dollars. This means that you can deduct your contributions from your taxable income, reducing your tax bill in the year that you make the contribution. However, you will have to pay taxes on your withdrawals in retirement at your ordinary income tax rate. Traditional IRAs also have RMDs, which means that you must start taking distributions from the account once you reach a certain age.

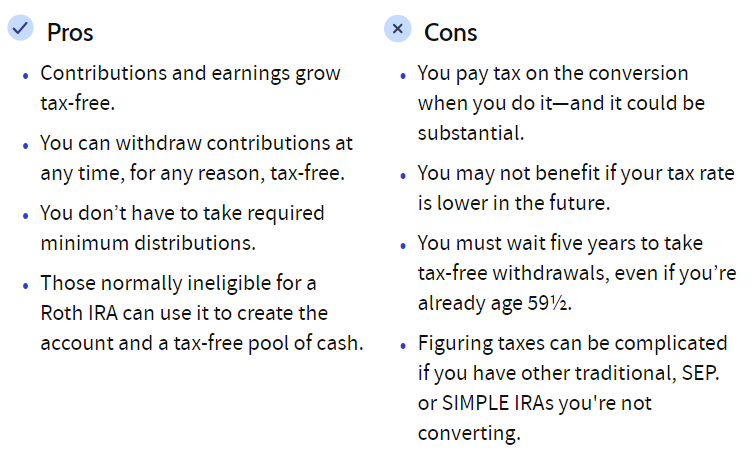

Pros and Cons of Roth IRAs

Pros

Tax-Free Withdrawals: One of the biggest advantages of a Roth IRA is that your withdrawals in retirement are tax-free. This can provide significant tax savings in the long run.

No Required Minimum Distributions: With a Roth IRA, you are not required to take distributions at a certain age, giving you more flexibility in managing your retirement savings.

Flexible Withdrawals: You can withdraw your contributions (but not your earnings) from a Roth IRA at any time penalty-free, making it a more flexible option for emergencies.

Cons

No Upfront Tax Deduction: Unlike a Traditional IRA, you do not get a tax deduction for your Roth IRA contributions, which means you miss out on potential tax savings in the present.

Income Limits: Roth IRAs have income limits that restrict high-income earners from contributing directly to the account.

Contribution Limits: The contribution limits for Roth IRAs are lower than Traditional IRAs, which can limit the amount you can save for retirement.

Pros and Cons of Traditional IRAs

Pros

Upfront Tax Deduction: Traditional IRAs allow you to deduct your contributions from your taxable income, reducing your tax bill in the year that you make the contribution.

Higher Contribution Limits: Traditional IRAs have higher contribution limits than Roth IRAs, allowing you to save more for retirement.

Spousal IRA: If you are a stay-at-home spouse, you can contribute to a Traditional IRA based on your spouse’s income.

Cons

Taxable Withdrawals: Your withdrawals from a Traditional IRA in retirement are taxed at your ordinary income tax rate, which can reduce the amount of money you have available for retirement.

Required Minimum Distributions: Traditional IRAs have RMDs, which means you must start taking distributions at a certain age, potentially reducing the growth of your retirement savings.

No Flexible Withdrawals: With a Traditional IRA, you may face penalties for withdrawing your money before age 59 ½, making it less flexible for emergencies.

Conclusion

Both Roth IRAs and Traditional IRAs have their own unique advantages and disadvantages. Ultimately, the best choice for you will depend on your individual financial situation and retirement goals. Consider factors such as your current tax bracket, expected future tax bracket, and investment timeline when deciding which type of IRA to contribute to. Consulting with a financial advisor can also help you make an informed decision about your retirement savings strategy. Whichever IRA you choose, the important thing is to start saving for retirement as early as possible to secure your financial future.